European construction sector set for moderate recovery in 2025

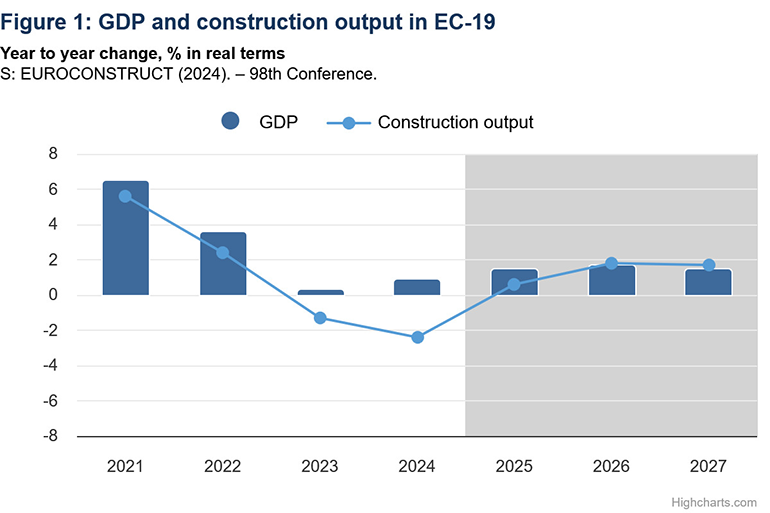

Euroconstruct estimates a 2.4% decline for the construction activity in Europe in 2024, followed by a slight growth of just +0.6% in 2025.

98th Euroconstruct Conference

The European construction market is going through a challenging period, marked by the persistence of external factors (e.g., the war in Ukraine), the effect of new one (the possible changes in US policy), as well as internal factors that continue to weigh on financial conditions (high interest rates and energy costs as well as increasing labour costs), that are hindering construction activity and investment plans. After a first decline in 2023, 2024 was the most difficult year for the industry since 2020. However, forecasts point to a positive turnaround from 2025 onwards.

This is in brief the picture that emerges from the survey presented during the 98th Euroconstruct conference held in Milan in December 2024 and hosted by Cresme.

Market Overview

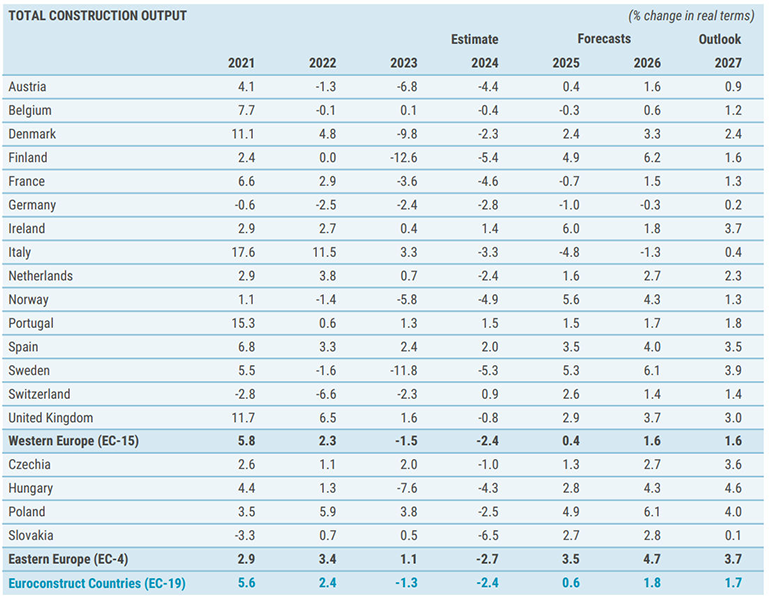

According to the new estimates, the construction activity in the 19 Euroconstruct countries is projected to decline by 2.4% in 2024, while a slight recovery is expected in 2025 with growth of just 0.6%, due to gain momentum in the following two years. This forecast represents a modest upward revision for 2024 by 0.3 percentage points compared to previous estimates, though the growth in 2025 is slightly weaker than initially anticipated, while the modest growth path for 2026 remains unchanged.

Residential Construction

The primary challenge for the European construction market in 2024 is the significant decline in new residential construction, following the one recorded in 2023. High property prices, still elevated interest rates (albeit declining) and high construction costs are the main obstacles. However, the sector is anticipated to stabilize in 2025, with growth accelerating in the following years. The residential renovation market is also in contraction, with a modest decline in 2024 and a further decrease in 2025 year. An improvement in the housing sector is forecast from 2026 onwards, driven by demographic factors, economic conditions and more favourable subsidy schemes for housing renovation.

Non-Residential Construction

The non-residential construction sector has faced challenges, with a modest decline experienced in 2023. This downward trend is expected to be confirmed in 2024, due to new non-residential construction projects that are under pressure. Despite these challenges, growth is projected to resume starting from 2025, with both new construction and renovation activities contributing positively to the overall non-residential construction sector. New investments will be particularly bright for the mainly public funded market segments, while incentives and structural policies targeting “green goals” will create consistent push for renovation activities across the sector.

Civil Engineering

Civil engineering remains a bright spot, driven by the urgent need for upgrades in transport networks and energy infrastructure. Investments in these areas are crucial to meet new demands and political goals. New civil engineering projects, after a weak 2024, are expected to grow significantly in the next two-year period, against a more stable and moderate development for renovation works, expected to be solid this year, with a gradual slowdown by the end of the forecast period.

Did you find this article useful?

Join the CWW community to receive the most important news from the global ceramic industry every two weeks

Related articles

Recent articles

Sirsi Valves accelerates its growth

Bruno Bettelli elected President of ACIMAC

Main topics

Read more